Main Facts: The Cooling of the Semiconductor Talent Market

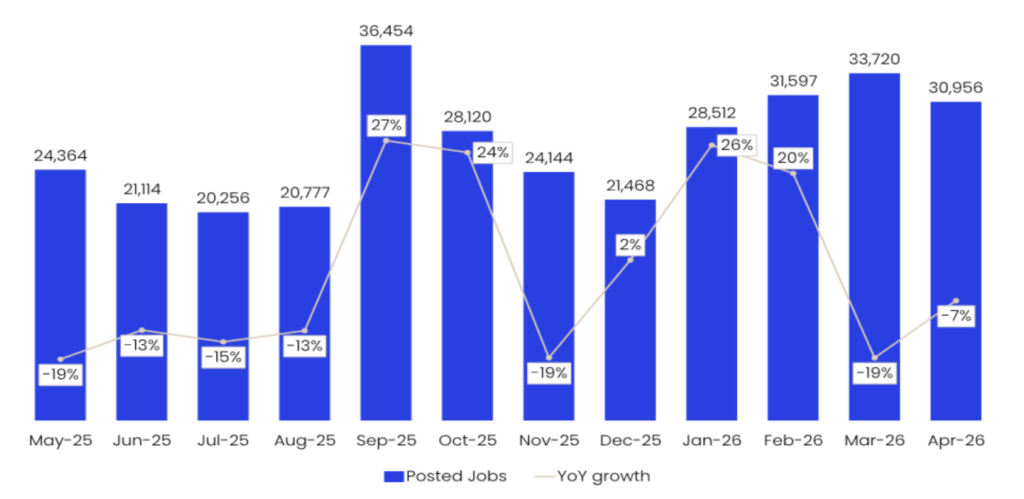

The global semiconductor talent acquisition market experienced a notable contraction in April 2026, signaling a shift in the investment strategies of major technology and manufacturing firms. According to the latest dataset from GlobalData Jobs Analytics, global job postings within the semiconductor sector fell by 6.58% month-on-month, dropping to a total of 30,956 active listings. This contraction follows a volatile first quarter characterized by aggressive hiring sprees, particularly during January and February.

For corporate executives, venture capitalists, and industry analysts, tracking workforce fluctuations serves as a highly reliable leading indicator. Hiring data acts as an early warning system for corporate performance, illustrating where companies are actively building capabilities or quietly scaling back long before these shifts manifest in quarterly earnings reports or sales figures. The 6.58% drop in April suggests that while the long-term demand for silicon remains robust, major players are entering a phase of consolidation and cost optimization.

Global Semiconductor Job Postings (Selected Milestones, 2025–2026)

| Month | Trend / Run-Rate Status |

|----------------|------------------------------------------------------|

| Mid-2025 | Market Trough (Lowest hiring activity of the cycle) |

| September 2025 | First Major Surge (Initial recovery phase) |

| December 2025 | Year-End Retrenchment (Baseline low point) |

| Jan–Feb 2026 | Q1 Acceleration Peak (Aggressive talent acquisition) |

| March 2026 | Initial Pullback (First signs of cooling) |

| April 2026 | Consolidation Phase (Postings ease to 30,956) |Despite this monthly pullback, the overall volume of active job postings remains higher than the troughs recorded in mid-2025 and the baseline lows of December 2025. This indicates that the current market environment represents a stabilization of hiring momentum rather than a structural downturn. Enterprise investments are continuing, but they are becoming increasingly targeted, with capital moving away from generalized expansion toward highly specific technical domains.

Chronology of the Semiconductor Talent Market (May 2025 – April 2026)

To understand the April 2026 cooling, it is necessary to examine the cyclical fluctuations of the preceding twelve months. The semiconductor talent market has been characterized by intense volatility, driven by macroeconomic pressures, shifting supply chain strategies, and the rapid evolution of artificial intelligence (AI) technologies.

Mid-2025: The Cyclical Trough

In the summer of 2025, the semiconductor hiring market hit a cyclical low. Following a period of oversupply in certain consumer-grade chip categories and high interest rates slowing venture capital, companies paused non-essential recruitment. Hiring run-rates during this period remained suppressed as firms focused on inventory digestion and operational efficiency.

September 2025: The First Step-Up

By late third quarter, hiring patterns shifted. September 2025 saw a sudden surge in job postings. This step-up was primarily driven by the expansion of domestic manufacturing initiatives in the United States and Europe (fueled by government subsidies like the CHIPS Act) and an escalating demand for specialized hardware capable of running next-generation AI models.

December 2025: Year-End Budget Consolidation

As is typical with corporate fiscal years drawing to a close, December 2025 witnessed a sharp retrenchment. Hiring activity fell back to baseline levels as human resources departments closed out active pipelines and finalized budgets for the upcoming year.

January – February 2026: The New Year Acceleration

The market experienced a massive resurgence in early 2026. January and February saw aggressive recruitment campaigns. Major hardware manufacturers and enterprise software giants competed fiercely for top-tier engineering talent, driving job postings to peak levels for the cycle.

March – April 2026: The Current Retrenchment

The hiring frenzy of early Q1 proved unsustainable. March 2026 marked the first step down, followed by the 6.58% contraction in April. This consecutive two-month decline indicates that corporations have filled their immediate critical vacancies and are now focusing on onboarding, integration, and capital preservation.

Supporting Data: Granular Analysis of the April 2026 Shift

The high-level decline in job postings masks a complex web of shifting priorities across technical themes, geographic regions, employer profiles, and required skill sets.

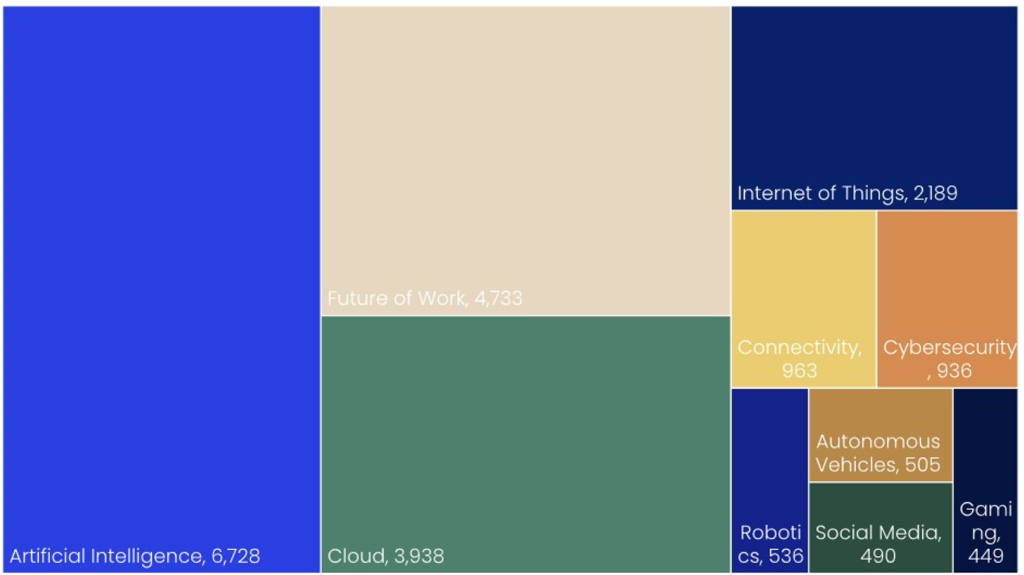

Thematic Hiring: AI and Cloud Dominate the Mix

Thematic analysis of the April 2026 data reveals that hiring is heavily concentrated in software-adjacent and digital modernization fields rather than pure-play hardware manufacturing.

- Artificial Intelligence (AI): Remains the undisputed leader with 6,728 active job postings. Companies continue to prioritize engineers capable of designing chips optimized for machine learning, neural networks, and large language models.

- Future of Work (FOW): Follows as the second-largest theme with 4,733 postings, reflecting the ongoing restructuring of corporate environments, hybrid collaboration tools, and automated enterprise workflows.

- Cloud Infrastructure: Comprises the third tier with 3,938 listings, driven by the continuous integration of cloud computing architectures with localized semiconductor systems.

Figure 2: Top Hiring Themes in the Semiconductor Sector (April 2026)

==================================================================

Artificial Intelligence (AI) [████████████████████████] 6,728

Future of Work (FOW) [█████████████████] 4,733

Cloud Infrastructure [██████████████] 3,938

Internet of Things (IoT) [████████] 2,189

Connectivity [███] 963

==================================================================Beyond these top three categories, there is a steep drop-off. Themes such as the Internet of Things (IoT) (2,189 postings) and Connectivity (963 postings) occupy a much smaller footprint. Highly publicized fields like autonomous vehicles, robotics, and gaming chips represent a very long, thin tail in terms of overall hiring volume.

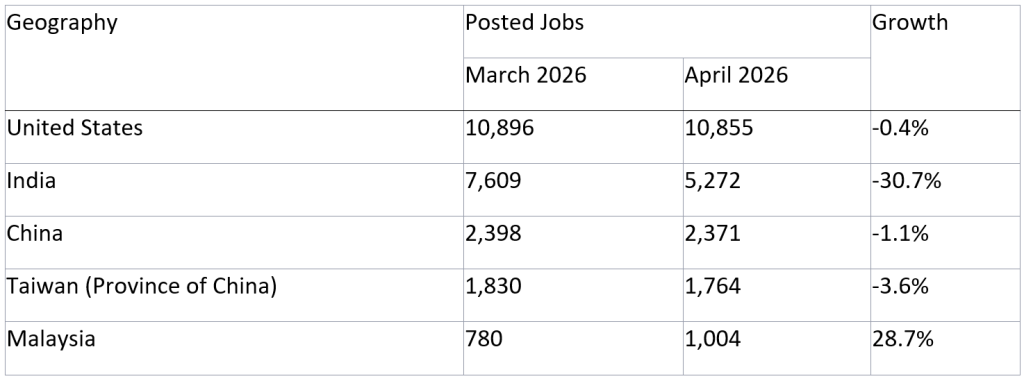

Geographic Shifts: Malaysia Surges as India Contracts

The geographic distribution of semiconductor hiring in April 2026 shows a stark divergence in national strategies and regional market dynamics.

Geographic Hiring Fluctuations (March 2026 vs. April 2026)

| Country / Region | MoM Change (%) | Market Characterization / Strategic Driver |

|--------------------|----------------|---------------------------------------------------------|

| United States | -0.4% | Flat; remains the dominant global hub for design & R&D |

| India | -30.7% | Sharp contraction; rationalization of offshore IT hubs |

| Taiwan | -3.6% | Moderate decline; stable advanced foundry operations |

| China | -1.1% | Minor easing; highly localized supply chain development |

| Malaysia | +28.7% | Rapid expansion; booming back-end packaging & assembly |The United States maintained its position as the largest absolute market for semiconductor recruitment, holding virtually flat with a minor MoM decline of just 0.4%. This stability underscores the U.S. market’s role as the primary hub for high-value research, chip design, and strategic corporate operations.

Conversely, India recorded the most significant negative swing, with job postings plummeting by 30.7% month-on-month. This sharp contraction suggests a sudden rationalization of offshore engineering centers and support roles as global firms rein in operational expenses.

East Asian semiconductor powerhouses China (-1.1%) and Taiwan (-3.6%) experienced modest, single-digit declines, pointing to steady operational baselines in fabrication and foundry management.

The standout positive performer was Malaysia, which registered a substantial 28.7% increase in job postings, reaching 1,004 active listings. This surge highlights Malaysia’s growing importance as a critical hub for back-end packaging, testing, and assembly—activities that are seeing renewed capital investment as companies seek to diversify their supply chains away from high-geopolitical-risk areas.

Employer Dynamics: Divergent Corporate Strategies

An examination of specific corporate hiring behaviors reveals highly individualized approaches to the current market environment.

- IBM: Despite remaining the largest overall job poster in April with 4,248 active listings, IBM has aggressively scaled back its recruitment velocity. This figure is down significantly from its peak of 9,517 in February and a subsequent 6,952 in March.

- Hitachi: Demonstrated remarkable stability, posting 2,300 active roles in April compared to 2,317 in March.

- Qualcomm & Huawei: Both companies bucked the broader cooling trend, recording moderate monthly increases to 1,203 and 917 postings, respectively.

- Jabil & Applied Materials: Experienced pullbacks, with Jabil dropping to 1,360 listings and Applied Materials easing to 904.

- Infineon: Emerged as a notable outlier, entering the top-employer list with 751 postings in April after registering zero active postings during the entire first quarter of 2026. This sudden spike points to a major, newly funded regional initiative or a rapid restructuring of its talent pipeline.

Technical Skills in Demand: Platform over Hardware

The specific technical competencies sought in April 2026 indicate that the semiconductor sector is increasingly prioritizing software integration over raw physical engineering.

The single most demanded skill category was Application Platforms and Containers (4,960 postings), reflecting the industry’s need for engineers who can containerize applications and manage microservices architectures. This was closely followed by Systems Design and Integration (3,637 postings) and Operating Systems (3,408 postings), highlighting the critical importance of low-level software compatibility and platform engineering.

Furthermore, a significant portion of active recruitment was dedicated to enterprise applications—such as application lifecycle management and HR/payroll systems—showing that semiconductor firms are actively upgrading their internal IT infrastructures to support global operations.

Official Responses and Industry Interpretations

The sudden shifts in the April 2026 data have drawn analysis from leading industry commentators and market researchers, who offer context on these fluctuating numbers.

GlobalData Analyst Commentary

In a briefing on the latest Jobs Analytics release, lead analysts noted that the cooling of semiconductor recruitment should not be interpreted as a sign of industry distress, but rather as a logical stabilization phase.

"We are seeing a transition from a frantic talent grab to a highly disciplined, strategic placement of capital," the report states. "In late 2025 and early 2026, companies were posting roles almost indiscriminately to secure scarce AI talent. What we are witnessing in April is the digestion of that talent. Organizations are now focused on building the software platforms, containerized environments, and systems integrations necessary to make their new hardware investments productive."

The Southeast Asian Re-shoring Narrative

Regional economic analysts have focused heavily on the diverging fortunes of India and Malaysia in the latest dataset. Economists specializing in Asia-Pacific supply chains suggest that Malaysia’s 28.7% surge is a direct result of the "China Plus One" strategy reaching maturity.

"For several years, multinational semiconductor firms have spoken about diversifying their packaging and testing footprints," noted one regional supply chain strategist. "The April data indicates that this talk has turned into real, on-the-ground execution. Malaysia’s established infrastructure in Penang and Kulim is attracting immediate hiring capital, while India’s massive engineering centers are experiencing a temporary digestion phase after years of rapid, high-volume expansion."

Strategic Implications for Corporate Leaders and Investors

The insights extracted from the April 2026 GlobalData Jobs Analytics report carry profound implications for executives, board members, and institutional investors across all sectors of the economy.

1. Hiring Data as a Critical Leading Indicator

For corporate strategists, relying solely on lagging financial indicators like quarterly earnings or backward-looking revenue reports is no longer sufficient. Job posting data has been proven to lead corporate earnings revisions by approximately one to three months.

By the time a competitor’s reduced hiring rate is discussed on an earnings call, their strategic pivot is already well underway. Leaders who monitor these talent signals in real-time can accurately predict which markets their rivals are entering, which products they are prioritizing, and where they are quietly retreating.

2. The Software-Defined Semiconductor Era

The heavy concentration of hiring in AI, Cloud, Application Platforms, and Systems Integration underscores a fundamental truth: the modern semiconductor industry is as much about software as it is about silicon.

Companies that design and manufacture chips must possess world-class platform engineering capabilities to ensure their hardware can be seamlessly integrated into cloud environments and AI workflows. For leaders in non-tech sectors, this trend highlights the necessity of developing internal software capabilities to effectively leverage next-generation silicon.

3. Navigating Geopolitical and Regional Talent Risks

The dramatic shift in hiring activity between India and Malaysia serves as a reminder of the volatility inherent in global talent supply chains. Organizations must remain agile, continuously evaluating their regional footprints.

Over-reliance on a single offshore market can expose a company to rapid wage inflation, localized talent shortages, or geopolitical disruptions. A balanced, multi-hub strategy—leveraging the distinct strengths of different regions (e.g., U.S. for high-concept design, Malaysia for advanced packaging, and localized hubs for software integration)—is critical for long-term operational resilience.

4. Capitalizing on Competitor Consolidation

The pullback in hiring by major players like IBM and Jabil presents a prime recruiting opportunity for mid-tier semiconductor firms and agile startups. During periods of aggressive talent acquisition by industry giants, smaller firms are often priced out of the market for specialized engineers.

The current cooling phase represents a strategic window for these organizations to secure elite technical talent that may be impacted by corporate consolidation or shifting institutional priorities.

In conclusion, while the April 2026 semiconductor hiring data points to a temporary cooling of momentum, it reveals a market that is maturing, professionalizing, and aligning its human capital with the practical realities of a software-driven, geopolitically diversified future. Leaders who can interpret these subtle talent signals will be uniquely positioned to make smarter, more proactive investment and operational decisions.